Signed into law in 2010, the Affordable Care Act was designed to extend health insurance coverage to as many Americans as possible. By its institution in 2013, it contained over 20,000 pages. It has only grown more complex over time, but some of the most important things to know are shown below.

What is the Affordable Care Act?

The Affordable Care Act ensures Americans who are not offered health insurance benefits through an employer are still covered affordably.

The affordability component is achieved through the issuing of subsidies, or tax credits.

How much do ACA plans cost per month?

It depends on a variety of factors. The biggest determinant of cost is your subsidy amount.

The formula for determining how much you have to pay each month is:

Full Cost of Plan – Your Subsidy Amount = Your Monthly Cost

What is a health insurance subsidy?

Subsidies are tax credits offered by the government that pay for some or all the cost of an insurance plan.

Unsubsidized plans tend to be fairly expensive, so it is definitely worth your time to check to see if you qualify.

How is a subsidy amount determined?

The formula for determining a health insurance subsidy is very complex. The two biggest factors are age and income. Some additional factors that impact the amount are county of residence, tax household size and the number of people applying for coverage.

I am eligible for Medicaid. Can I get an ACA plan instead?

If you are currently eligible or enrolled in Medicaid, it is your best option. Medicaid eligibility prevents you from being eligible for an ACA subsidy.

Is there an income requirement to qualify for a subsidy?

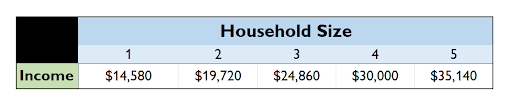

If you project that your household income will be less than 100% of the Federal Poverty Limit (shown below), you are not eligible for a subsidy and should instead enroll in Medicaid.

The greater your projected income is past the above figures, the higher your monthly cost for coverage will be. For example, if your income is $30,000 with a household size of 1, your policy will be less expensive than someone whose income is $50,000 if all other factors stay the same.

My employer offers coverage but it’s expensive. Can I get a subsidy and cheaper insurance with an ACA plan?

Unfortunately, if you are offered coverage through an employer, you are not eligible for a subsidy. Even if you don’t like your plan offerings, you are still disqualified from subsidy eligibility.

If you are offered coverage through a spouse’s employer plan, you are also ineligible, unless it is too expensive to meet the affordability threshold. More information is included in the question below.

I am not offered employer-coverage but my spouse is. Can I still get a subsidy for an ACA plan?

Not in most cases. Unfortunately if you are offered employer coverage through a spouse, it precludes you from getting subsidized coverage independently.

The one exception is if the plan through your spouse fails to meet the affordability threshold. If the cost of you and your dependents (if applicable) enrolling in the plan would cost greater than 9.12% of your household income, it is considered unaffordable and you are eligible for a subsidy through the ACA Marketplace.

If you feel like you may qualify for this exception, please reach out to our team at 252-495-8965 for more information.

What is the easiest way to see how much of a subsidy I qualify for?

My subsidy amount is showing up as $0 and the plans are very expensive. What can I do?

Call our office at 252-495-8956.